📍 Update Location

About Me

Alex Monito Nhancololo

Ph.D. student in Statistics and Probability

A. M. Nhancololo is a Ph.D. student in Statistics and Probability at the Institute of Mathematics, Statistics and Computer Science, University of São Paulo (IME–USP), advised by Prof. Airlane Pereira Alencar. He is currently (01/01 - 30/06, 2026) a visiting researcher at Jaume I University, advised by Prof. Jorge Mateu.

He holds an M.Sc. in Statistics and Agricultural Experimentation from the Federal University of Lavras (UFLA), advised by Prof. João Domingos Scalon, where he received the Best Thesis Award (2024). He earned his Bachelor of Education in Mathematics with a specialization in Statistics from Universidade Save, advised by Prof. André Silvestre Cuinica.

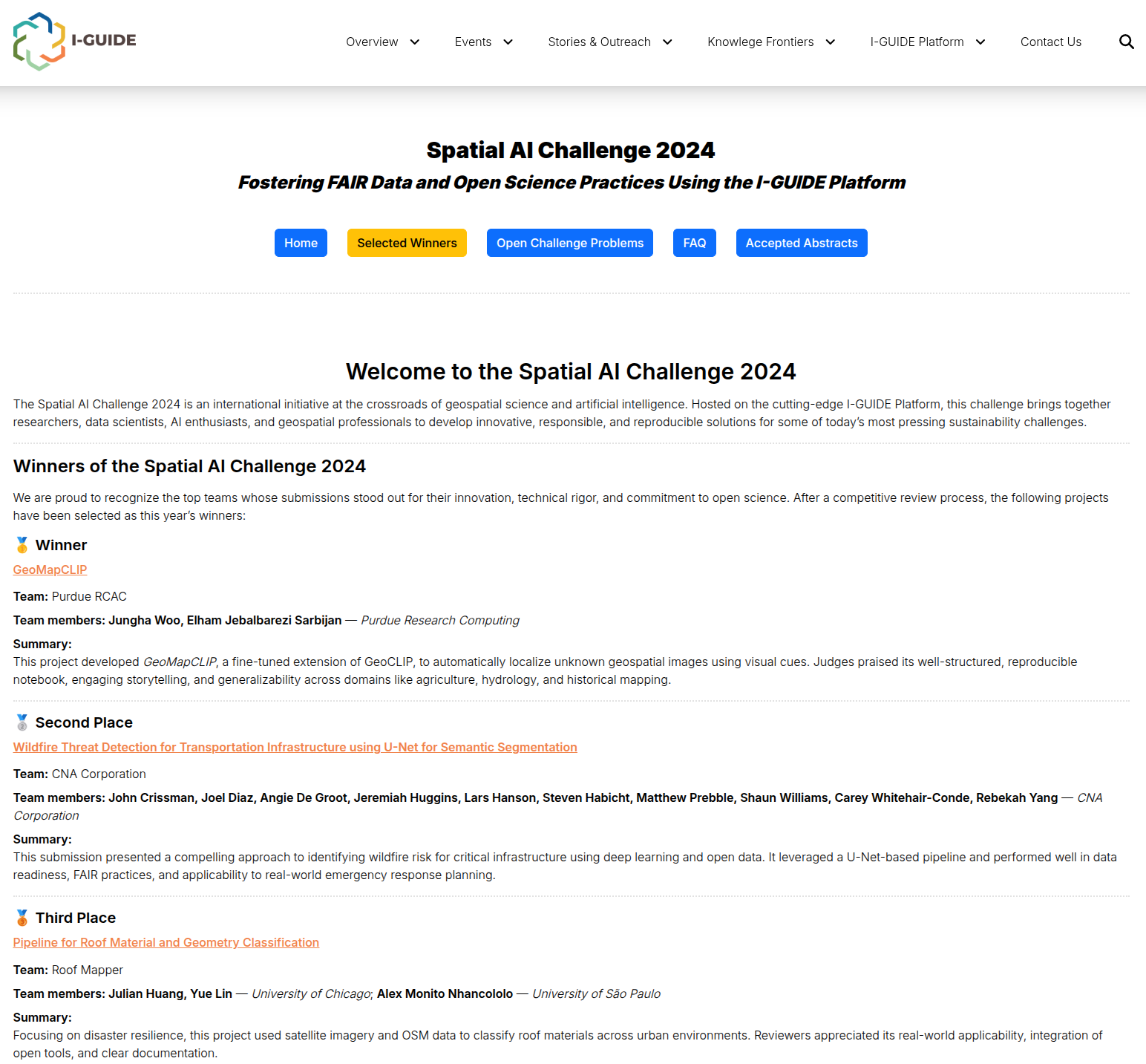

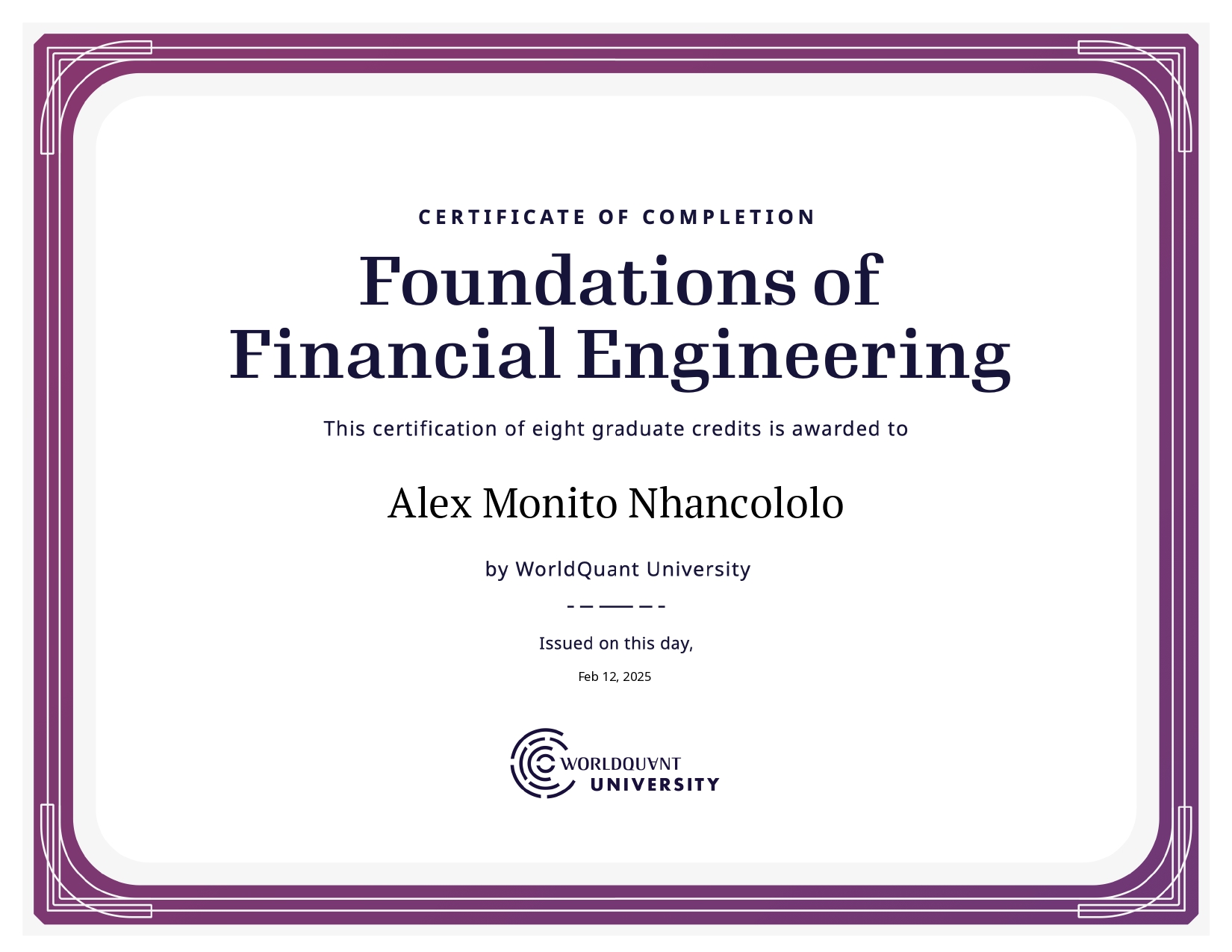

Additionally, he is pursuing an M.Sc. in Financial Engineering at WorldQuant University and an MBA in Artificial Intelligence and Big Data at the Institute of Mathematical and Computer Sciences, University of São Paulo (ICMC–USP), advised by Prof. Caetano T. Júnior. He was awarded third place in the Spatial AI Challenge 2024 (I-GUIDE), alongside Julian Huang and Yue Lin (University of Chicago).

His primary research interests lie in spatio-temporal statistics and their applications to the social sciences, environmental studies, ecology, agriculture, and medicine. Methodologically, his work focuses on geospatial intelligence (GeoAI), spatial point processes, lattice/area data, and geostatistics.

Honors & Awards

Spatial AI Challenge 2024

Awarded third place in the Spatial AI Challenge 2024 (I-GUIDE), together with Julian Huang and Yue Lin (University of Chicago).

2024 Best Master’s Thesis Award in Statistics

Award for the Best Master’s Thesis in Statistics, defended in 2024.

Foundations of Financial Engineering

- Applied linear algebra and Python for filtering, summarizing, and transforming structured and unstructured financial data

- Prepared datasets for econometrics, machine learning, and deep learning models

- Conducted quantitative analysis of financial risks including credit risk, volatility, and liquidity

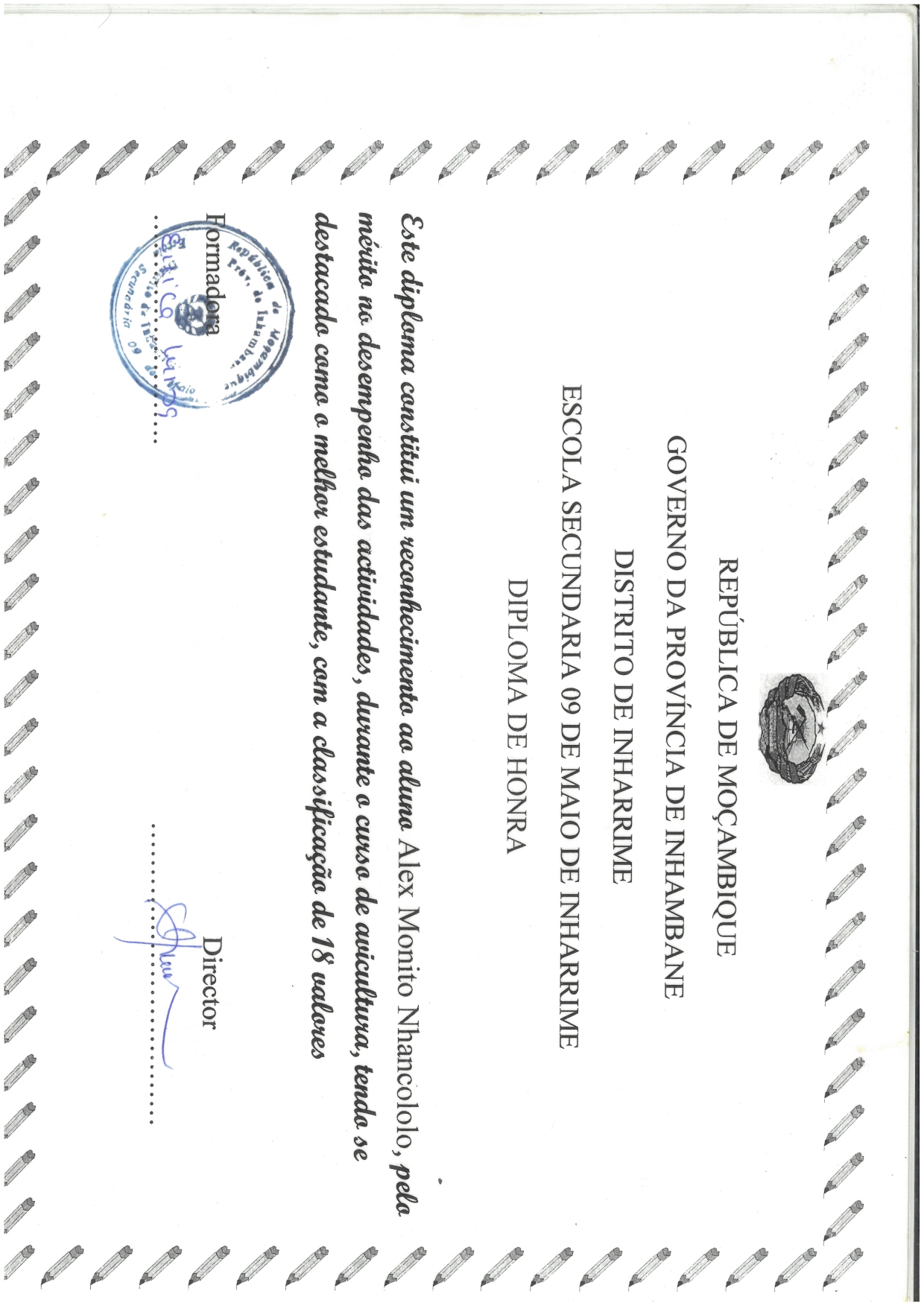

Poultry Production

Outstanding Student in the Poultry Production Course